The second part is the date of record that determines who receives the dividends, and the third part is the date of payment, which is the date that payments are made. Printing Plus has $100 of dividends with a debit balance on the adjusted trial balance. The closing entry will credit Dividends and debit Retained Earnings. Regularly closing your books will prevent unwanted changes from occurring to your accounting data after you generate important financial reports for your accountant or tax professional. Some accounting software automatically closes your income and expense accounts at year-end before adding your net profit (or loss) to your retained earnings account. Accounting software may create an automatic closing date as well as a password so transactions from before the closing date can’t be changed.

Why You Can Trust Finance Strategists

Both closing entries are acceptable and both result in the same outcome. All temporary accounts eventually get closed to retained earnings and are presented on the balance sheet. Closing all temporary accounts to the retained earnings account is faster than using the income summary account method because it saves a step. There is no need to close temporary accounts to another temporary account (income summary account) in order to then close that again. Permanent accounts track activities that extend beyond the current accounting period.

Credits & Deductions

After the closing journal entry, the balance on the drawings account is zero, and the capital account has been reduced by 1,300. These temporary or “nominal” accounts are zeroed out and reset when closing entries are added to an accounting system so they don’t affect the next accounting period. Sum your general ledger accounts again to take into account the adjusted entries from the last step, and then add them all together to make a new trial balance, making sure your debits and credits are again equal. Adjusting entries record items that aren’t noted in daily transactions. These items include accumulation (known as “accrual” in accounting) of real estate taxes or depreciation accrual, which need to be recorded to close the books. Post the account totals from your cash payments and your sales and cash receipts journal to the appropriate general ledger account to close the books.

Step 2: Clear expenses to the income summary account

Remember the income statement is like a moving picture of a business, reporting revenues and expenses for a period of time (usually a year). We want income statements to start every year from zero, but for accounts like equipment, debt, and cash accounts—reported on the balance sheet—we want to keep a running balance from the beginning of the business. Now that all the temporary accounts are closed, the income summary account should have a balance equal to the net income shown on Paul’s income statement. Now Paul must close the income summary account to retained earnings in the next step of the closing entries. Temporary accounts, also known as nominal accounts, are accounts that track financial transactions and activities over a specific accounting period. These accounts are “temporary” because they start each accounting period with a zero balance and are used to accumulate data for that period only.

Temporary and Permanent Accounts

- Both closing and opening entries record transactions, but there is a slight variation in their purpose.

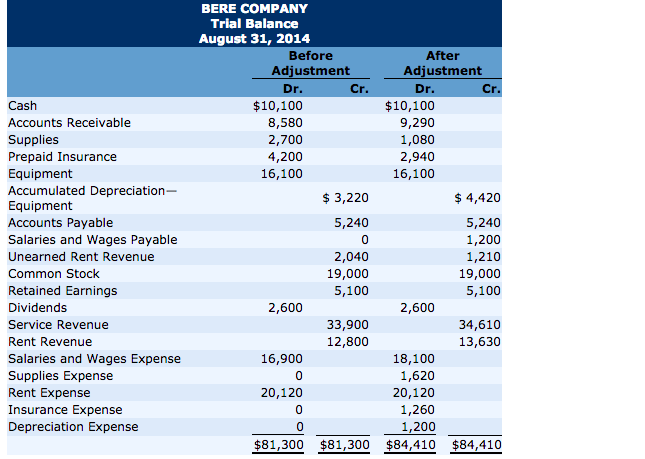

- Once we have made the adjusting entries for the entire accounting year, we have obtained the adjusted trial balance, which reflects an accurate and fair view of the bakery’s financial position.

- The closing entry entails debiting income summary and crediting retained earnings when a company’s revenues are greater than its expenses.

- The purpose of closing entries is to transfer the balances from temporary accounts (revenues, expenses, dividends, and withdrawals) to a permanent account (retained earnings or owner’s equity).

The Retained Earnings account balance is currently a credit of $4,665. In this chapter, we complete the final steps (steps 8 and 9) of the accounting cycle, the closing process. You will notice that we do not cover step 10, reversing entries. This is an optional step in the accounting cycle that you will learn about in future courses. Steps 1 through 4 were covered in Analyzing and Recording Transactions and Steps 5 through 7 were covered in The Adjustment Process.

Which accounts are closed at the end of an accounting period?

The post-closing T-accounts will be transferred to the post-closing trial balance, which is step 9 in the accounting cycle. You might be asking yourself, “is the reserve accounting wikipedia Income Summary account even necessary? ” Could we just close out revenues and expenses directly into retained earnings and not have this extra temporary account?

In contrast, temporary accounts capture transactions and activities for a specific period and require resetting to zero with closing entries. Closing entries are a fundamental part of accounting, essential for resetting temporary accounts and ensuring accurate financial records for the next period. This process highlights a company’s financial performance and position.

Since the income summary account is only a transitional account, it is also acceptable to close directly to the retained earnings account and bypass the income summary account entirely. These finalized reports show a business’s financial position over a certain accounting period—whether a month or an entire year. Automation transforms the process of closing entries in accounting, making it more efficient and accurate. By leveraging automated systems, businesses can ensure that all tasks related to closing entries are handled seamlessly, reducing manual effort and minimizing errors.

Shaun Conrad is a Certified Public Accountant and CPA exam expert with a passion for teaching. After almost a decade of experience in public accounting, he created MyAccountingCourse.com to help people learn accounting & finance, pass the CPA exam, and start their career. Net income is the portion of gross income that’s left over after all expenses have been met. The term “net” relates to what’s left of a balance after deductions have been made from it.

Note that by doing this, it is already deducted from Retained Earnings (a capital account), hence will not require a closing entry. Temporary accounts can either be closed directly to the retained earnings account or to an intermediate account called the income summary account. The income summary account is then closed to the retained earnings account. No, permanent accounts carry their balances forward to the next accounting period. A net loss would decrease retained earnings so we would do the opposite in this journal entry by debiting Retained Earnings and crediting Income Summary.